Taxaly

Designed a 0→1 AI-assisted tax planning tool that helps people who hate taxes understand and act on their tax decisions before the year is over, not discover the outcome at filing time.

ROLE

Product Design Intern

TEAM

1 Product Designer, 1 Financial Advisor, 1 Data Scientist, 4 Developers

FOCUS AREA

Engagement Strategy

Behavior Design

Product Experience

TIMELINE

Dec 2025 - May 2026

A SHIFT IN TIMING

From Reporting to Planning

Most tax tools look backward. Taxaly was built to plan forward.

Reporting the Past

Most tax tools help you report what already happened. You gather last year's documents, enter numbers, and find out what you owe or what you're getting back. By then, it's too late to change anything.

Shaping the Outcome

Taxaly needed to do the opposite: help people plan their taxes before the year unfolds, shifting from a once-a-year scramble to proactive decisions that reduce what you owe, not just calculate it.

THE VISIBILITY GAP

What Does Planning Forward Actually Change?

Forward-looking tax planning makes impact visible before the year ends, when adjustments still matter.

APRIL: REACTIVE REALITY

Earning $80,000/yr as a full-time employee.

Taxes are deducted automatically. You only discover the outcome during filing season.

TAX OWED

$1,200

LOCKED

JANUARY: THE INTERVENTION

Rewind to planning and intervention.

Increase 401(k) contribution by $5,000 throughout the year.

TAXABLE INCOME

DROP

TAX LIABILITY

REDUCED

TAX OWED

$300

$900 SAVED

The decision wasn't complicated. It was just invisible.

THE REAL CHALLENGE

Designing for Confidence,

Not Calculation

When we started shaping Taxaly, the challenge wasn’t building tax calculations. It was designing for people who don’t fully understand what applies to them, yet still have to make high-impact financial decision especially salaried professionals navigating investments, equity, and side income.

WHAT WE OBSERVED

This wasn’t just a usability issue.

It was a trust issue

Through early competitive analysis, journey mapping, and conversations with a financial advisor, a few patterns became clear:

Outcomes come too late

Users only see their total owed or refund amount at filing time, long after opportunities to adjust contributions, withholdings, or deductions have passed.

Knowledge is assumed

Most tools expect users to understand terms like “safe harbor,” “estimated payments,” or contribution limits, without clarifying how they apply personally.

Simplicity hides trade-offs

“Streamlined” flows prioritize speed over visibility, collapsing complex decisions into single recommendations without showing alternatives.

Unclear consequences create hesitation

When users can’t see how one decision affects the rest of their tax picture, they hesitate, or default to doing nothing.

WHERE THIS LED US

Tax planning operates under uncertainty.

Income shifts throughout the year. Contribution limits vary. Eligibility rules depend on individual circumstances.

INCOME

Isn't fixed

DEDUCTIONS

Aren't universal

LIMITS

Aren't intuitive

ELIGIBILITY

Changes by profile

In that context, optimizing for speed or minimal interaction would have been misleading

01

The system needed to make cause and effect visible.

02

Users needed to see how a decision changed their outcome before committing to it.

Taxaly wasn’t about simplifying taxes.

It was about designing for confidence under uncertainty.

THE TURNING POINT

Why I Pushed Back

on a Fully Conversational Product

The team was excited about building something fully conversational. It aligned with the broader shift toward AI-first interfaces. It was clean, bold, and easy to articulate: “Just talk to your taxes.”

It was compelling. It was modern. But when I mapped real planning scenarios, adjusting withholdings, modeling 401(k) contributions, the gaps became obvious.

In a domain defined by uncertainty, removing structure didn’t reduce anxiety. It removed control.

In a purely conversational flow:

Users couldn’t see their full tax picture at a glance.

Comparing “before vs after” required scrolling through history.

Recommendations appeared authoritative, but reasoning wasn't visible.

There was no stable surface for users to review and validate decisions.

"I wasn’t convinced that conversation alone could support real financial decisions."

Proposing a hybrid model meant pushing against momentum.

I knew a hybrid approach would feel less novel. It risked feeling less ambitious. But as we walked through real user scenarios, the trade-off became harder to ignore.

STRATEGIC PIVOT

"The goal wasn’t to prove we could build an AI interface. It was to design something people could trust with real money decisions."

THE SYSTEM WE BUILT

A Hybrid Planning Experience

The hybrid decision gave the product a direction. But the real work was designing how conversation and structure worked together, while addressing timing, visibility, trust, and assumed knowledge across the entire system.

Four Experience Pillars

That Shaped the Product

01

Plan Before It’s Too Late

02

Make Impact Visible

03

Guide Without Taking Control

04

Teach in Context

ONBOARDING

Before You Can Plan Forward,

You Need a Clear Baseline

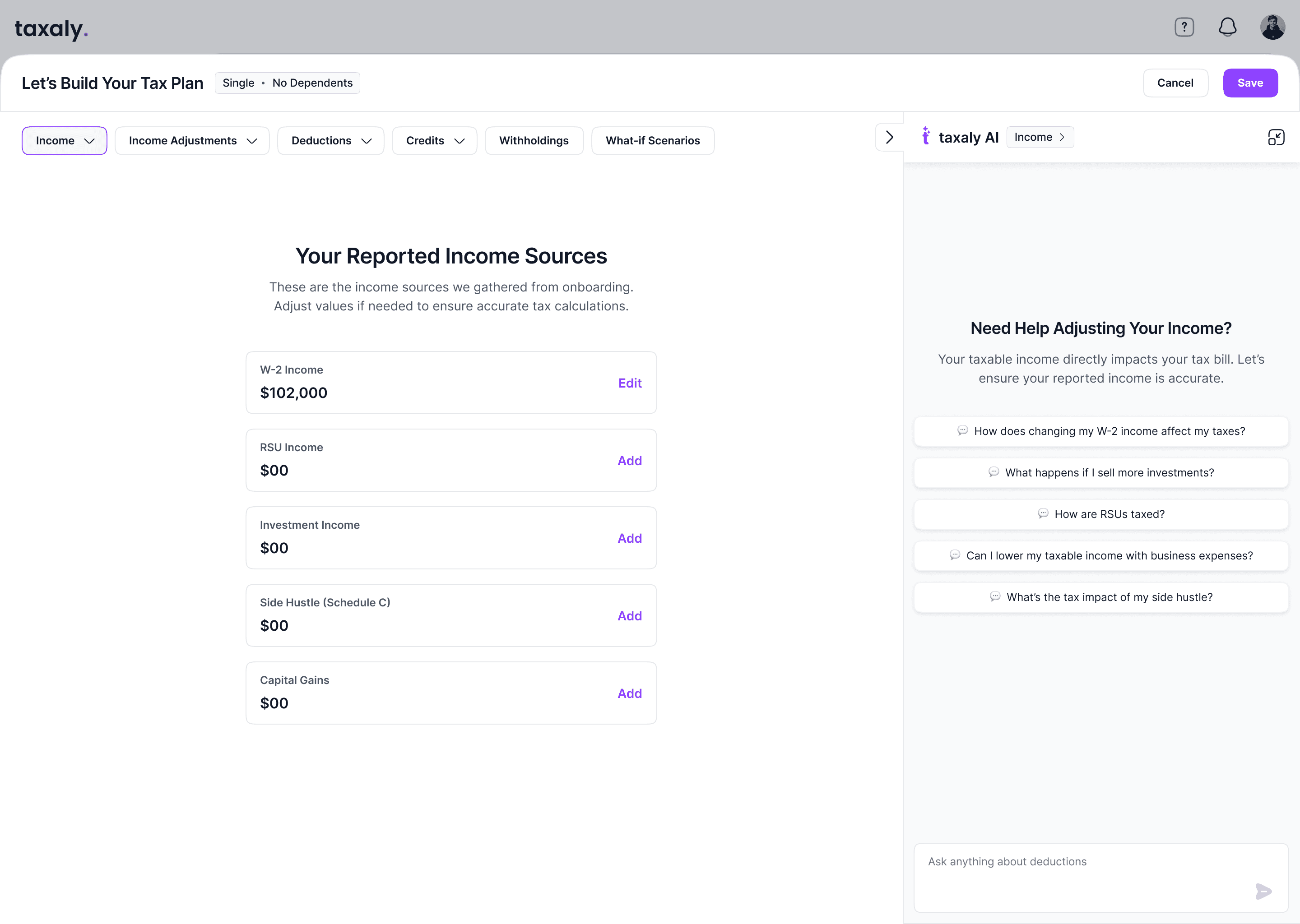

Before modeling decisions or suggesting adjustments, we needed a reliable starting point. This setup builds the financial foundation for the year ahead.

Make Critical Decisions Visible

Filing status isn’t a minor detail, it changes tax brackets, eligibility, and planning strategy. We surfaced it early to prevent hidden assumptions from shaping the outcome. Because this was an MVP, we intentionally supported the most common filing statuses first. Instead of hiding unavailable options, we surfaced them transparently and allowed users to opt in for updates.

Build the Year in Context

Collect What Matters, Nothing More

THE BASELINE

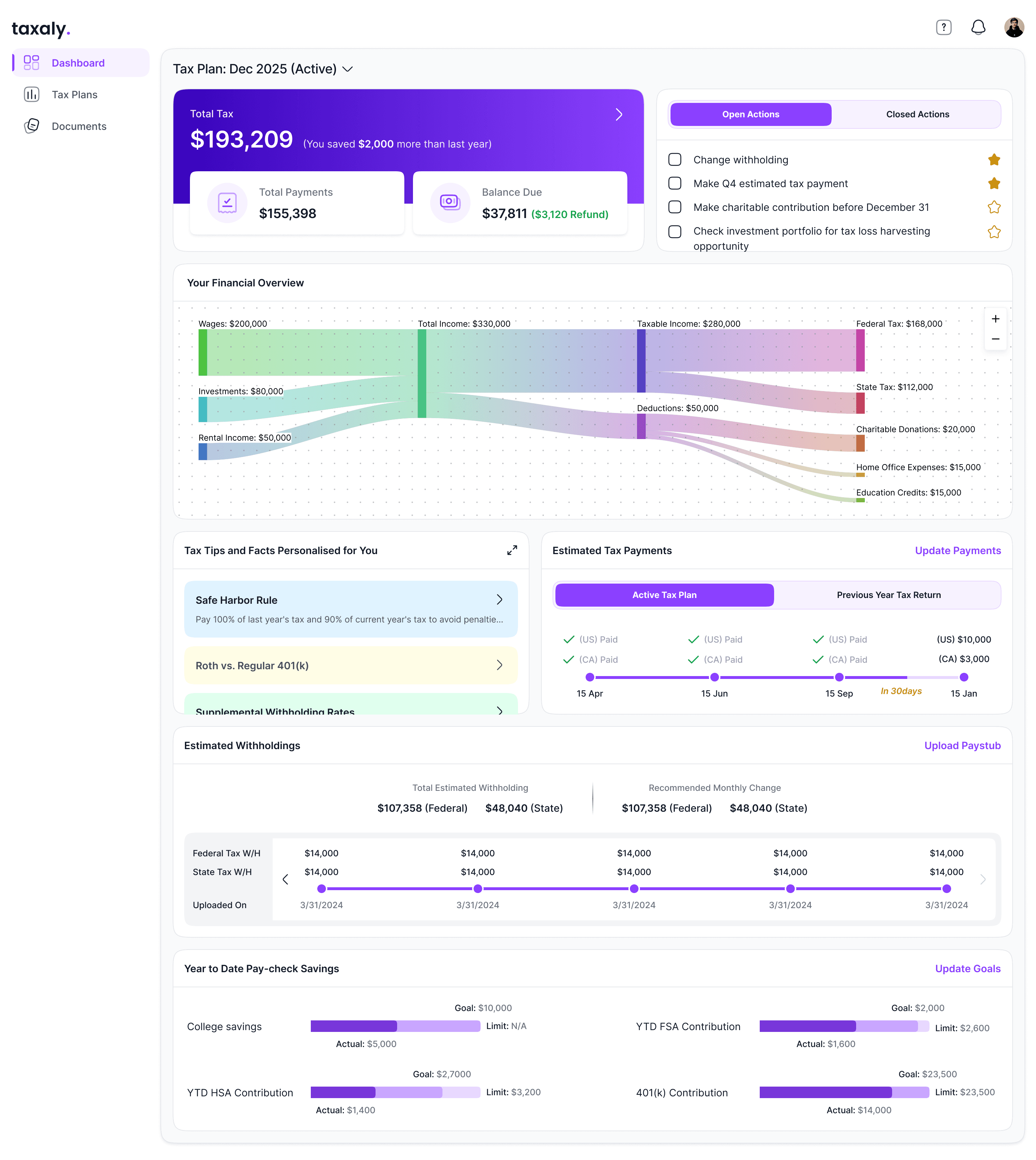

Your Year, Made Visible

Based on the information provided, the system generates a live snapshot of the current year, not a final outcome, but a starting point.

Total tax is calculated

in real time

Income flows into taxable

income transparently

Open actions highlight decisions that can still change the outcome

Balancing transparency with cognitive load was a key tension. We chose to surface complexity, but layered it progressively through drill-downs and contextual explanations.

The dashboard wasn’t static. Every number could be explored, adjusted, or understood in context.

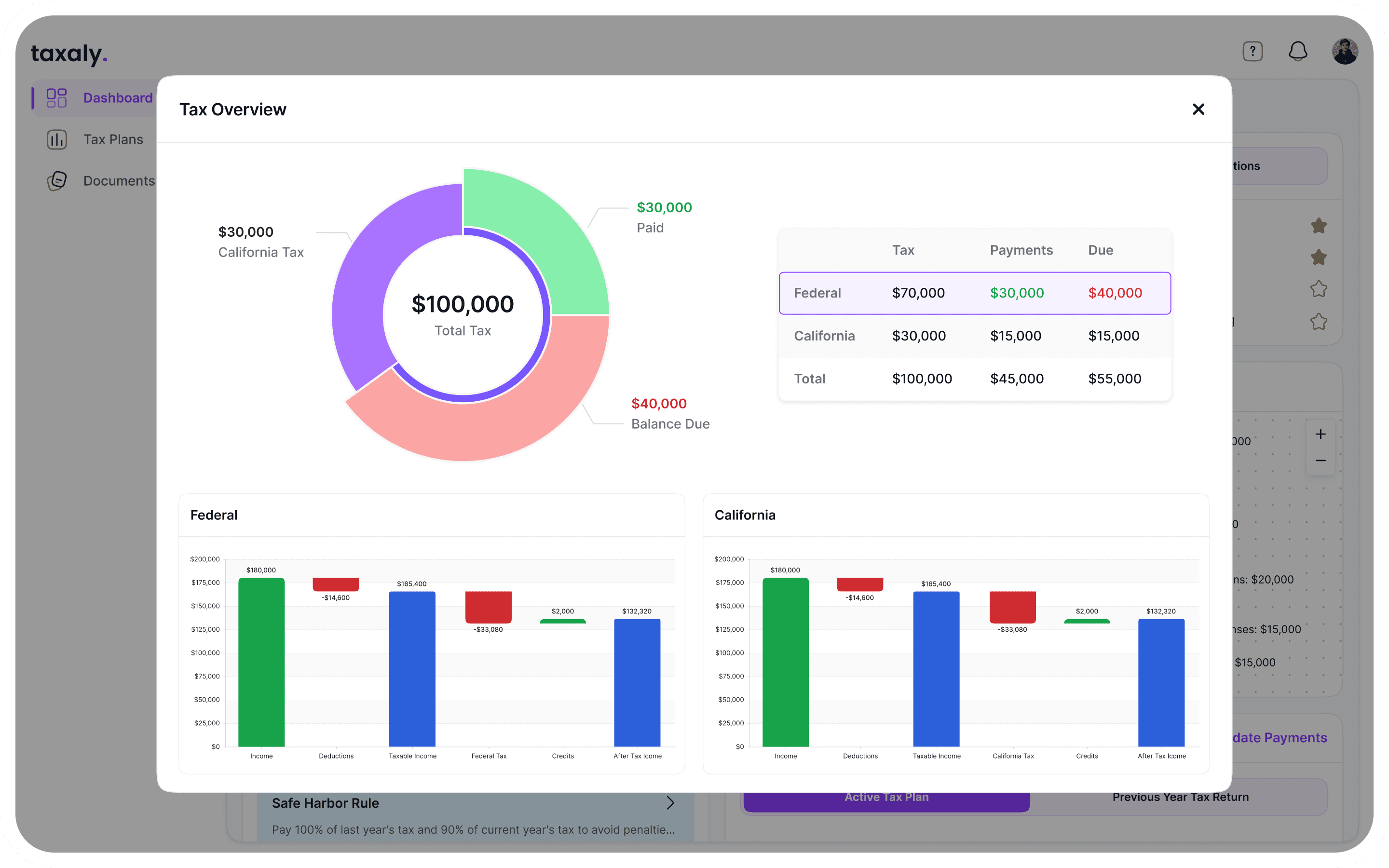

See Where the Number Comes From

Users can drill into federal and state components to understand how income, deductions, and credits shape the total. Nothing is presented as a black box.

Adjust Before It’s Too Late

Explain Without Assuming Knowledge

THE SHIFT FROM VIEWING TO SHAPING

What Happens If You Change Something?

Once users had a clear baseline, the product stopped being a dashboard.

It became a decision environment. Tax planning isn’t a single adjustment. It’s a layered system.

Income

ADJUSTMENTS + DEDCUTIONS

Lower Your Taxable Income

Tax Calculated

Before Credits

CREDITS

Credits Reduce the Tax

Final Tax Owed

WITHHOLDINS + ESTIMATED PAYMENTS

What You Already Paid

Refund

If you paid more than you owe

Balance Due

If you paid less than you owe

Taxaly didn’t simplify this complexity away. It made it explorable.

Meet Aggy

Aggy is a 27-year-old product designer earning $102,000 a year. His paycheck feels steady. Predictable. Last year, he still owed $1,800 in April, and didn’t see it coming. This year, he logs in early, while there’s still time to change the outcome.

BASELINE SNAPSHOT

February 12, 2026 — projecting the full 2026 tax year

PROJECTED 2026 TOTAL TAX

$19,600

PROJECTED 2026 WITHHOLDING

$17,900

IF NOTHING CHANGES

$1,700

Due in April 2027

Let's See How Aggy Changes This

That $1,700 doesn't disappear on its own.

Aggy won't make one big move. He'll move through the plan the way most people actually do, checking, adjusting, and watching the number respond. One step at a time

01 — INCOME

Is This Income Accurate?

Before changing anything, Aggy checks what the system is using to calculate his taxes.

W-2 income

$102,000

RSUs

None

Investment income

None

Side hustle

None

The inputs are accurate.

PROJECTED BALANCE REMAINS

$1,700 due

No change from baseline yet. But this step matters.

Before shaping the plan, Aggy confirms the inputs are correct.

01 — INCOME

Is This Income Accurate?

Before changing anything, Aggy checks what the system is using to calculate his taxes.

W-2 income

$102,000

RSUs

None

Investment income

None

Side hustle

None

The inputs are accurate.

PROJECTED BALANCE REMAINS

$1,700 due

No change from baseline yet. But this step matters.

Before shaping the plan, Aggy confirms the inputs are correct.